Tax Considerations for Your Incentive Stock Options

Key Points

Equity compensation plans, or long-term incentive plans, have become increasingly complex to understand. There are many different forms, each with its own unique set of risks, potential rewards, and tax implications.

Incentive Stock Options are similar to Non-Qualified Stock Options with the exception of potential preferential tax treatment.

While Incentive Stock Options can provide tax benefits, an exercise could also trigger additional taxes under the Alternative Minimum Tax (although changes in recent tax law makes this unlikely).

“A salary makes you a living, but profits make you a fortune.”

This saying is very applicable when you analyze a corporate executive’s sources of compensation. They may be paid a handsome salary, but in many cases, it’s their long-term incentive plan that truly builds wealth. How much wealth executives can build from their long-term incentive plans depends largely on how well they understand each plan’s structure.

Equity compensation plans, or long-term incentive plans, have become increasingly complex, making them hard to understand. There are many different forms, each with its own unique set of risks, potential rewards, and tax implications.

We’ve previously discussed various types of equity compensation plans, including Non-Qualified Stock Options. We’ll now discuss and compare another type of stock option compensation called Incentive Stock Options.

How Incentive Stock Options Are Similar to Non-Qualified Stock Options

As with a Non-Qualified Stock Option (NSOs), Incentive Stock Options (ISOs) are a form of executive compensation that is offered with the goal of retaining key employees. There are four basic facets to ISOs:

ISOs allow an employee the ability to purchase company stock at a specified “grant” price.

ISOs are subject to similar vesting schedules which must be satisfied prior to exercising the options.

There are no tax implications at either grant or vesting dates.

Once the ISOs have vested, they can be exercised in a similar fashion to NSOs, either through a straight cash purchase, stock swap, or “cashless transaction.” More on cashless transactions in a minute.

How Incentive Stock Options Are Different from Non-Qualified Stock Options

Incentive Stock Options are “qualified” stock options, which means they receive preferential tax treatment upon exercise. Unlike NSOs, ISOs do not require the employee to pay higher ordinary income tax on the “bargain element,” which is the difference between the grant price and the exercise price. Instead, the employee will pay a lower tax on long-term capital gains — provided they follow certain disposition rules.

There are two types of disposition rules:

1) Qualifying Disposition: Sale of the stock two years after the grant date and one year after the options were exercised.

2) Disqualifying Disposition: Any form of stock sale that does not meet the qualifying disposition’s holding period.

If the employee meets the Qualifying Disposition rule, they will only pay tax on long-term capital gains on the entire transaction. Otherwise, they will have to report ordinary income on the “bargain element,” turning the ISO into an NSO.

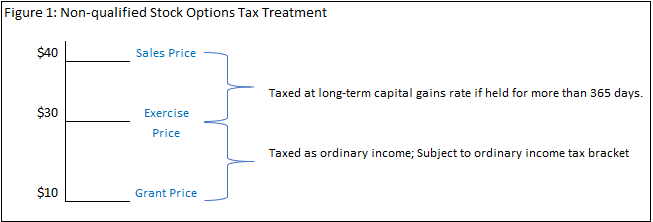

See Figure 1 and Figure 2 below, which compare the tax treatment of an NSO and an ISO (with a Qualifying Disposition).

How to Receive Preferential Tax Treatment on ISOs

To fully benefit from the qualified status of an ISO, care must be taken to meet the Qualifying Disposition rule. Many individuals make the mistake of using what is called a “cashless exercise” when exercising their ISOs. As the name implies, a cashless exercise is an option exercise where no cash is required from the employee. Instead, shares from the option grant are sold to cover the exercise costs. At this point, the transaction immediately becomes a Disqualifying Disposition because shares are sold at the time of exercise and not postponed to at least one year after exercise.

In order to meet the second part of the Qualifying Disposition rule, individuals exercising ISOs should instead use cash to pay for the option cost and fees/commissions. As an alternative, they could also initiate a stock swap where they surrender existing shares to cover the option costs and fees/commissions. This, of course, requires an individual to own the stock outright in a separate account.

How Exercising ISOs Impacts the Alternative Minimum Tax (AMT)

Exercising ISOs can impact the calculation of the Alternative Minimum Tax (AMT). The bargain element on an ISO has to be added back into income during the AMT calculation because it is considered a “preference item.” It is a preference item because you are only paying long-term capital gains on the bargain element. Although the ISO exercise could trigger additional taxes from the AMT, changes in the recent tax law will likely all but eliminate the tax.

Key Take-Away

Incentive Stock Options represent a major benefit that employers offer to their key employees. Not only is there potential for an employee to purchase company stock at a bargain price, but there are also opportunities to recognize this income at lower tax rates, relative to other long-term incentive plans. Just remember to exercise your options using a cash purchase or stock swap to keep it as a Qualifying Disposition.

If you have any questions about ISOs, how they fit into your overall portfolio, ideal times to exercise, AMT impact, or any other considerations, please contact one of our Wealth Advisors. We welcome the opportunity to analyze your portfolio to identify your asset allocation with the ISOs, prepare a tax projection to show the AMT impact, and discuss any other concerns. Learn more with Capstone Financial Advisors.

Disclosures:

This article is not a substitute for personalized advice from Capstone and nothing contained in this presentation is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. This article is current only as of the date on which it was sent. The statements and opinions expressed are, however, subject to change without notice based on market and other conditions and may differ from opinions expressed by other businesses and activities of Capstone. Descriptions of Capstone’s process and strategies are based on general practice, and we may make exceptions in specific cases. A copy of our current written disclosure statement discussing our advisory services and fees is available for your review upon request.